DSCR Loan Pre-Submission Checklist — 8 Things to Confirm Before You Apply

Current DSCR pre-submission requirements investors should verify before sending a deal to a lender.

Don't Submit Blindly

Most DSCR deal problems don't start at the lender's desk. They start in the investor's spreadsheet — before anyone has even pulled a credit report or ordered an appraisal.

A deal that looks clean at first pass often looks different once a lender runs their own numbers. They'll recalculate income using a rent schedule from a licensed appraiser, not your Zillow comp. They'll plug in projected post-purchase taxes, not the current bill. They'll use their own insurance benchmark if you can't produce an actual quote. They'll apply their underwriting rate — which may be higher than the rate they quoted you. And they'll look at what happens to your ratio when any one of those inputs moves against you.

By the time the lender flags a problem, you've already burned time, ordered reports, and possibly committed earnest money. The purpose of this page is to help you find the problems first.

The six verification areas below map directly to the DSCR Pre-Submission Checklist — the same go/no-go framework I use before recommending a deal moves forward.

Different Property Types. Different Risks Before Submission.

A clean DSCR submission is not one-size-fits-all. A stabilized Brooklyn building, a free-market acquisition, and a 5+ unit property can all be viable — but each one needs a different underwriting check before it reaches a lender.

Rent-Stabilized Multifamily

Before submission, stabilized properties often need a deeper look at refinance survivability and lender risk tolerance.

- DSCR compression analysis

- Expense stress testing

- Hold vs. sell evaluation

- Lender overlay review

- Restructure path analysis

Free-Market Multifamily

Free-market investors usually need to know whether the deal is strong enough before they submit, refinance, or scale.

- Acquisition filtering

- Leverage optimization

- Refinance analysis

- Market comparison review

- Lender-ready packaging

5–10 Unit Properties

Once a property moves above four units, the review becomes more commercial-style and documentation-driven.

- Rent roll review

- T12 expense review

- Occupancy and NOI analysis

- Commercial DSCR evaluation

- Submission package readiness

1. Rent Verification Requirements

Rent is the numerator in your DSCR equation, which means any inflation in that number inflates your ratio and makes a marginal deal look like a pass. Lenders know this. The appraiser's rent schedule will almost always come in lower than your projected number — and when it does, your DSCR compresses in ways that can kill an approval you were counting on.

What to verify:

Pull conservative rent comps from StreetEasy or Rentometer using the same unit count, within ±0.25 miles, from the last 90 days. That's your benchmark. Your projected rent needs to be compared to that number, not to last year's actuals or a neighbor's lease.

Calculate the rent gap — the percentage difference between your projected gross rent and the conservative comp rent. A gap under 10% means your projections are defensible. A gap over 15% means the appraiser will likely come in lower than your number, and your DSCR will compress at the worst possible moment.

Recalculate your DSCR using the conservative comp rent, not your projection. If that conservative DSCR falls below 1.15, your deal's approval is appraiser-dependent. You may still close — but you're exposed to a single data point outside your control. Factor vacancy at a minimum of 5%, meaning effective rent is gross rent × 0.95.

2. Tax Verification Requirements

Property tax documentation is one of the most commonly missing items in a DSCR deal file. Current NYC property tax rates from the NYC Department of Finance give lenders the verified annual tax figure they need to calculate PITIA accurately — a number that directly affects the qualifying DSCR ratio. This is where NYC investors get burned most often, and it's almost always avoidable. The current tax bill on the listing is not the tax bill the lender is going to use — and it's not the tax bill you're going to pay after the sale closes.

What to verify:

Property taxes in New York City are subject to reassessment after a sale. For Class 2 investment properties, the post-purchase projected tax is estimated as: Purchase Price × 0.45 × 0.125. That's the number to use in your DSCR calculation — not the current tax bill you see in the listing.

Calculate the gap between the current tax bill and your projected post-purchase tax. That gap, annualized, tells you how much additional expense you're absorbing — and how much pressure it adds to your debt service coverage.

Confirm which number your lender uses. Some lenders underwrite to current taxes. Some use projected. Some use whichever is higher. That single policy decision can change your qualifying DSCR by 0.05–0.15 depending on the deal size.

3. Insurance Verification Requirements

Insurance is the expense item investors most often underestimate. Using a rough estimate or a number from a previous deal on a different property type isn't enough — not for your analysis, and not for lender underwriting.

What to verify:

Get an actual broker quote before you run your final DSCR. Frame construction, masonry, older buildings with prior claims, and mixed-use properties all price differently, and the spread between property types can be significant. The benchmarks below are per-unit starting points for NYC investment properties — your actual quote may vary based on coverage level, deductible structure, and building-specific factors.

Insurance cost benchmarks (per unit/year):

| Property Type | Benchmark / Unit |

|---|---|

| Frame, standard | $1,800 – $2,200 |

| Frame, older / prior claims | $2,200 – $2,800 |

| Masonry | $1,500 – $1,900 |

| Mixed-use | $2,500 – $3,200 |

Also confirm the lender's minimum coverage requirement and maximum allowable deductible before you bind a policy. Being under-insured on coverage or over the deductible cap can delay your close or require a policy revision.

4. Rate & Debt Service Requirements

The rate a lender quotes you is not always the rate they'll use to calculate your DSCR. And even if they use the quoted rate for underwriting, the rate environment between application and closing can move — and it can move enough to flip a marginal deal into a decline.

What to verify:

Confirm the lender's underwriting rate. This is the rate they plug into their debt service calculation, and it may be higher than your quoted note rate. If the spread between quoted and underwriting rate is more than 0.25%, recalculate your DSCR using the underwriting rate before you submit — not after.

Run rate sensitivity. Every 0.25% increase in rate adds roughly Loan Amount × 0.00021 to your monthly P&I payment. Calculate your DSCR at your quoted rate and again at +0.50%. If the +0.50% DSCR drops below the lender's minimum, your deal is rate-sensitive and you need to know that before it surprises you at rate lock.

Confirm your rate lock strategy — timing, lock period length, and extension cost. A 30-day lock on a deal that takes 45 days to close costs real money and creates real pressure. Know the options before you're in the middle of them.

Finally, calculate your DSCR buffer above the lender's stated minimum. The minimum gets you in the door. The buffer tells you how much margin you actually have if anything moves.

5. Stress Test Requirements

A deal that clears the lender minimum at current assumptions is not necessarily a deal worth doing. The base case is what the market looks like today. Your hold period is what it looks like for the next three to seven years. Stress testing tells you how much room you actually have before the deal stops working.

What to verify:

Run four scenarios and record every result. This is your deal's actual risk profile — not an optimistic projection, not a worst-case fear. It's the math.

Stress test matrix:

| Scenario | Calculation | Threshold |

|---|---|---|

| Base Case | Current assumptions | — |

| Rent −10% | Rent × 0.90 | DSCR > 1.25 |

| Taxes +30% | Taxes × 1.30 | DSCR > 1.25 |

| Rate +0.50% | Rate + 0.50% | DSCR > 1.25 |

| Combined (worst 2) | Apply two stresses above | DSCR > 1.00 |

Every single stress should hold above 1.25 — NYC market conditions demand a higher buffer than national DSCR benchmarks. The combined scenario — applying the two most damaging stresses simultaneously — should stay above 1.00. If it doesn't, you need to know your breaking point before you submit. Specifically: at what rent drop does the deal fail, and at what tax increase does it fail? Those aren't academic questions. They're the numbers that determine how much risk you're actually taking on.

If you want to run these scenarios on a live deal, use the Stress Test tool.

6. Go / No-Go Submission Decision

After you've worked through the five verification areas above, the decision logic is straightforward. It's not a judgment call. It's a score.

Seven criteria. Each one is a yes or a no. If all seven are yes, the deal is ready to submit. If one or two are no, fix them before the lender sees the file — not after. If three or more are no, you have a structural deal problem. Renegotiate the terms or walk.

The seven criteria:

Rent gap < 15% and DSCR recalculated at conservative comp rent

Taxes modeled using post-purchase projected number, not current bill

Actual insurance quote obtained and compared to benchmark

DSCR clears lender minimum with a buffer of at least 0.10

All single stress tests pass above 1.25 (NYC standard)

Combined stress test passes above 1.00

Rate lock strategy confirmed — timing, period, and extension cost known

Use the checklist below to work through each criterion against your actual deal numbers before you submit.

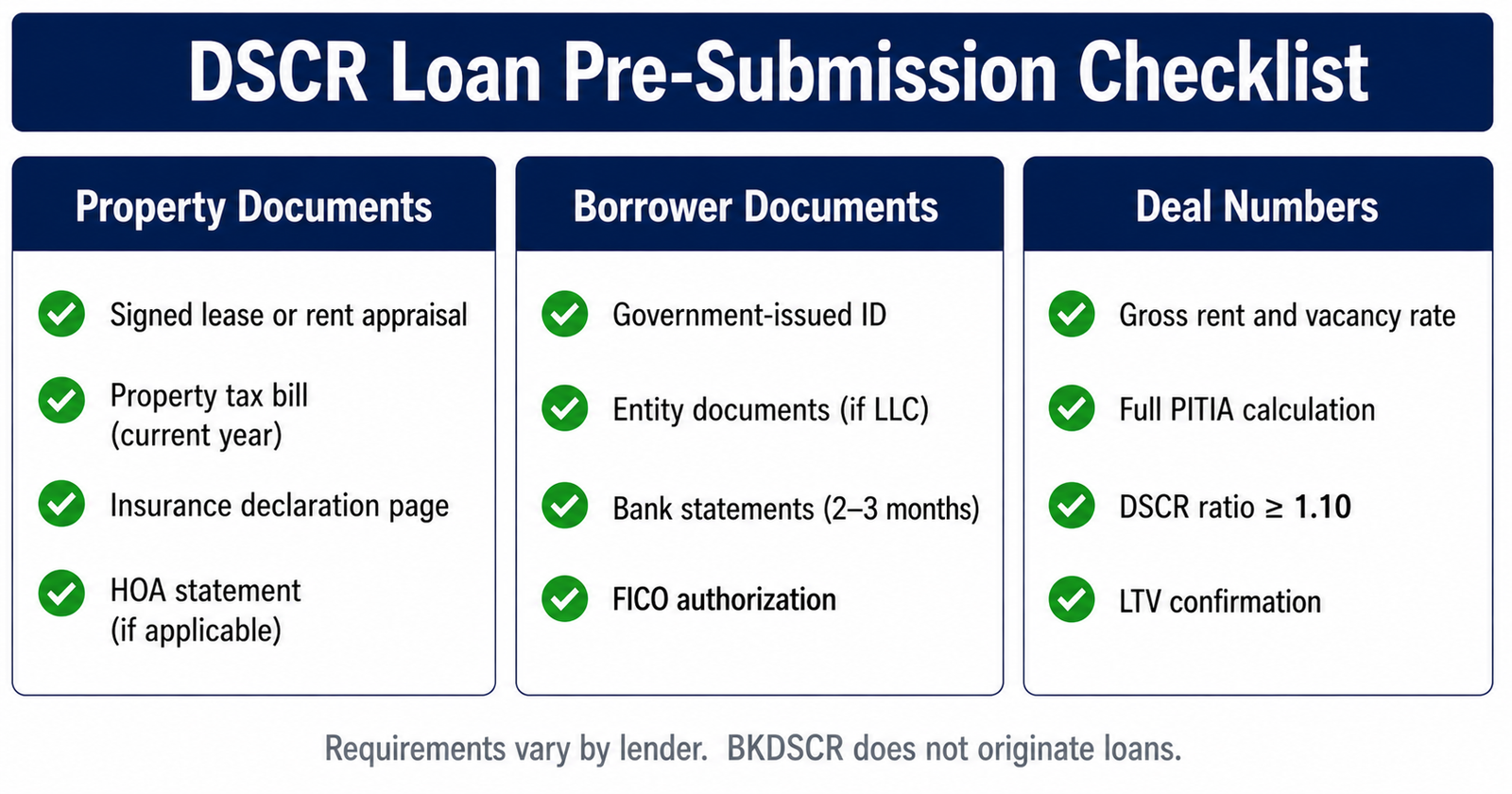

Download the DSCR Pre-Submission Checklist

Before you submit your deal to a lender, use this checklist to verify the rent, taxes, insurance, DSCR buffer, rate sensitivity, and stress-test results. Formulas, benchmarks, and go/no-go thresholds included.

Download the Checklist →Run Your Deal Through the Tools First

The checklist works faster when the math is already done. These tools cover the key calculations before you sit down with a lender.

60-Second Deal Filter →

Fast go/no-go on income, expenses, and DSCR before you commit time to a full analysis.

Run the Deal FilterDSCR Stress Test →

Model rent drops, tax increases, and rate movement against your deal's current ratio.

Run the Stress TestDSCR Calculator →

Calculate your ratio at quoted rate, underwriting rate, and conservative rent in one place.

Calculate the DSCRLender Criteria →

Understand what lenders evaluate beyond the ratio: overlays, property rules, and borrower factors.

Review Lender CriteriaWant a Second Set of Eyes Before You Submit?

If your deal passes the checklist but you still want confirmation from someone who's done this 100+ times, request a deal review before sending the file to a lender. No pitch. Just honest feedback on whether the deal actually qualifies, what your biggest risk is, and which lender fits your situation.

Or keep working the numbers:

Run the 60-Second Deal Filter →

Download the Pre-Submission Checklist →

Want the full scope in one document? Download the DSCR Playbook.

No Hype. Just Real Numbers.