DSCR Deal Review NYC — Written Analysis Before You Talk to a Lender

Submit your deal. Get a full lender-style analysis delivered to your inbox within 48–72 hours.

Most investors don't have a deal problem.

They have a financing reality problem.

A property can look strong on paper — cash flow positive, good rent, solid location — and still get denied by a lender. Not because the deal is bad. Because it wasn't reviewed the way a lender actually underwrites it.

That's exactly what this process fixes.

DSCR loan growth in investment property lending has accelerated since 2022 — making a pre-lender deal review more valuable as more investors enter the market without a clear picture of how their numbers will look at underwriting.

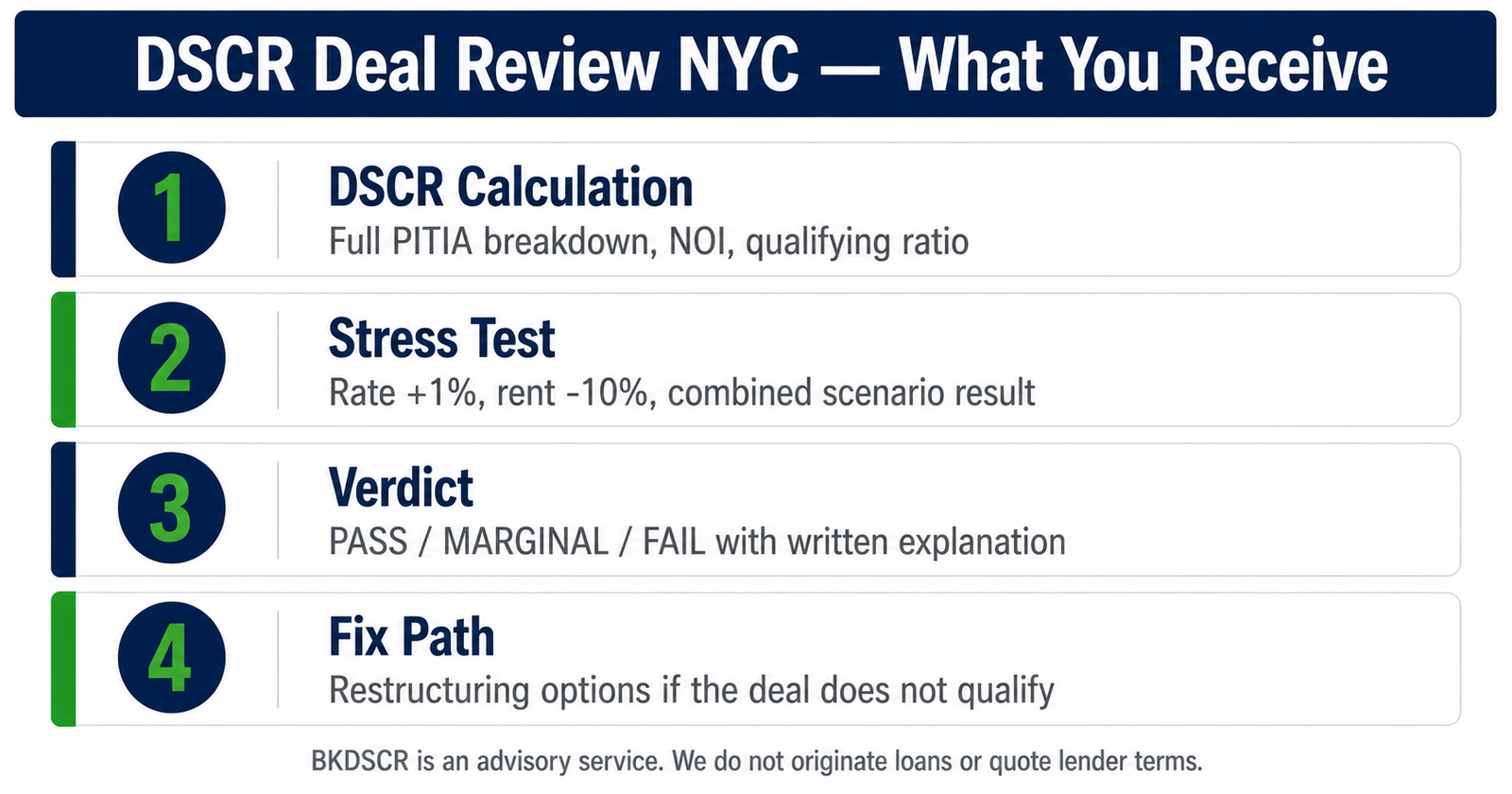

Your DSCR Deal Analysis Report — What You Receive

- Submit your deal numbers using the client intake form below

- We run a full lender-style DSCR analysis on your deal

- Your deal review report lands in your inbox within 48–72 hours

- No phone call required — the report tells you exactly where you stand

- Questions after reviewing? Reply directly to the delivery email or book a call

Submit your deal once. Get the same lender-style analysis back — no strings attached.

This free deal review is available once per investor. Returning clients can access deal reviews through our paid service.

No commitment. No obligation. No sales pitch.

If the deal qualifies, and you're not already working with a lender, I can introduce you to a BKDSCR partner lender.

If it doesn't, we show you exactly how to fix it.

Disclosure: BKDSCR may receive compensation from partner lenders when an introduction results in a closed loan. Lender introductions are made only when a deal qualifies independently through our review process.

Why Real Estate Deals Get Rejected by Lenders

Most deals fail because they were never reviewed the way a lender actually looks at them.

- Incorrect DSCR calculations

- Overestimated rental income

- Underestimated operating expenses

- Weak or missing stress testing

- Submitting to the wrong lender for the deal profile

This process catches those issues before a lender does — before you waste a credit pull, lose a rate lock, or kill a deal that could have closed.

No hype. Just real numbers.

How the DSCR Deal Review NYC Process Works

Complete the Client Intake Form

Enter your deal numbers — property details, rents, expenses, loan structure. The form takes 5–10 minutes. No bank login. No documents to upload.

Qualification required — use the checklist below to confirm this process is the right fit before submitting.

We Run the Analysis (48–72 Hours)

Your deal is run through a full lender-style underwriting model — DSCR calculations, PITIA analysis, stress testing, expense validation, and lender overlay.

This is the same framework a serious DSCR lender applies before they approve or deny.

Your Report Is Delivered by Email

A deal review report lands in your inbox with a clear verdict, full breakdown, risk flags, and specific next steps — no call required to interpret it.

Reply to the email with questions or book a call if you want to go deeper.

Two Possible Outcomes — Both Are Useful

We Connect You With a Partner DSCR Lender

If the deal clears lender-style underwriting and you're not already working with a lender, I can introduce you to a BKDSCR partner lender matched to your deal profile.

You go into that conversation knowing exactly where your deal stands — DSCR, LTV, cash flow, risk flags — and with a report that backs it up.

Disclosure: BKDSCR may receive compensation from partner lenders when an introduction results in a closed loan. Lender introductions are made only when a deal qualifies independently through our review process.

We Show You Exactly How to Fix It

If the deal doesn't qualify as structured, the report tells you exactly why — in real dollar terms — with the specific gap flagged. Fix paths and restructuring options are available as a paid next step.

A deal that fails today doesn't have to fail next month.

What the DSCR Deal Review Covers — 6 Core Sections

Full DSCR Analysis

Multiple DSCR calculations including the PITIA DSCR — the primary metric lenders use — not just the investor-view number.

Lender-Style Underwriting

Your deal reviewed through the same framework a lender applies: stressed vacancy, stressed rate, actual expense loading, and NOI validation.

Stress Test Results

Seven stress scenarios — rate increases, rent drops, vacancy spikes, expense shocks — tested against your actual deal numbers.

Risk Flags & Fix Paths

Every flag that could cause a denial — tax risk, insurance risk, rent risk, rate risk — identified with specific remedies if needed.

Lender Fit Analysis

The deal is tested against real lender profiles to identify the right submission lane and flag any gaps before you apply.

Clear Verdict + Next Step

Pass, marginal, or fail — stated plainly. No vague conclusions. No jargon. A specific action you can take after reading the report.

Real Deals. Real Numbers.

Every deal below was submitted by an NYC investor who thought they knew where they stood. The review changed the outcome.

Investor's DSCR: 1.18 → BKDSCR Conservative DSCR: 1.04 → After Restructure: 1.27

Investor thought he was at 1.18 and ready to submit. Our conservative model — which loads management, maintenance, and actual taxes — came in at 1.04. That's a MARGINAL, not a pass. Taxes were underloaded by $380/month off the listing sheet. We confirmed market rents, corrected the expense stack, and renegotiated the purchase price. Restructured DSCR cleared our 1.25 threshold. Submitted and closed.

Investor's DSCR: 1.21 → BKDSCR Conservative DSCR: 0.94 → After Restructure: 1.26

Investor was confident at 1.21. Our number was 0.94 — a hard fail. Commercial vacancy was loaded wrong and insurance was quoted, not actual. Both fixable. Purchase price came down $35K. Expense stack corrected. Restructured DSCR hit 1.26 — just over our 1.25 floor, with enough margin to hold if rates tick up. Closed.

Investor's DSCR: 1.31 → BKDSCR Conservative DSCR: 0.88

Investor calculated 1.31 and was 48 hours from submitting. Our conservative model came in at 0.88 — a deal that fails at the lender's floor, not just ours. A pending tax reassessment added $6,200/year to the expense load — not in his numbers at all. We stopped the submission before he burned a hard credit pull on a deal that needed full restructuring first. That's exactly what this process is for.

Before You Submit — Confirm You're in the Right Place

This process is built for experienced investors running income-producing rental properties. Answer the four questions below to confirm it's the right fit for your deal.

Quick Qualification Checklist

Check all four boxes to unlock the intake form.

Check all four boxes to unlock the intake form.

Submit Your Deal for DSCR Review

Complete the client intake form. Your deal review report will be delivered to your inbox within 48–72 hours.

No commitment. No obligation. No sales pitch.

Most deals that get denied were submittable. They just needed the right pre-submission prep.

Complete the Qualification Checklist Above →After submitting, you'll receive a confirmation email. Your PDF report follows within 48–72 hours.

Questions? Reply to the delivery email or schedule a call.

Submitting an unreviewed deal to a lender costs more than time. A denial triggers a hard credit pull, can kill a rate lock, and flags the deal for future lenders. Most of these issues are preventable — if the deal is run correctly before submission.

This process exists to catch those issues first. That's it.

FAQ

Is this a loan application?

No. This is a pre-submission deal review — an independent analysis run before you ever approach a lender. No credit pull. No application. No obligation.

How do I receive the results?

Your deal review report is delivered as a PDF to the email address you provide on the intake form, within 48–72 hours of submission. The report includes your full DSCR analysis, verdict, risk flags, and recommended next steps. No phone call required — though you're welcome to reply to the delivery email or schedule a call if you want to go deeper.

What if my deal doesn't qualify?

The report tells you exactly why it doesn't qualify — in real dollar terms — and flags the specific gap. From there, the Full Deal Breakdown + Strategy is the paid next step — that's where the fix paths live: purchase price reduction, loan restructuring, rent verification, a different lender lane. A deal that fails today doesn't have to fail next month.

What if my deal does qualify?

If you're not already working with a lender, I can introduce you to a BKDSCR partner lender matched to your deal profile. You go into that conversation with a full analysis in hand — DSCR, cash flow, stress results, risk flags — and a report that backs up your numbers.

Disclosure: BKDSCR may receive compensation from partner lenders when an introduction results in a closed loan. Lender introductions are made only when a deal qualifies independently through our review process.

What information do I need to submit?

Property address, purchase price or current value, rent roll, annual taxes and insurance, loan structure (down payment %, rate, term), and any known expenses. The intake form walks you through each section. Most investors complete it in under 10 minutes.

Is this only for NYC properties?

The process is built specifically for NYC outer-borough investors — Brooklyn, Queens, and the Bronx — because NYC has market-specific dynamics (tax structure, insurance environment, rent regulations, vacancy benchmarks) that require different underwriting assumptions than other markets. If your property is outside NYC, this review may not reflect accurate local benchmarks.

What happens after the review?

You read the report, assess the verdict, and decide your next move. If you have questions, reply to the delivery email. If you want to talk through the findings or explore lender options, book a call. There is no pressure, no upsell, and no follow-up unless you initiate it.

About This Process

BKDSCR is an education and advisory platform built exclusively for experienced NYC outer-borough investors — Brooklyn, Queens, and the Bronx — focused entirely on DSCR lending. No loan origination. No mortgage brokering. No conflicts of interest.

This framework is built on 25+ years of rental investing and mortgage lending experience — by someone who has been on your side of the table and understands how lenders evaluate deals from the inside.

The analysis isn't produced by a calculator. It's a full lender-style underwriting model run on your specific numbers, with a report written to tell you exactly what they mean and what to do next.

One purpose: catch deal issues before the lender does.

No Hype. Just Real Numbers.

BKDSCR is an independent DSCR education and advisory platform. We do not originate loans or act as a mortgage broker. BKDSCR may receive compensation from partner lenders when a client introduction results in a closed loan. This does not affect the independence of our analysis or deal review process.