You’ve already calculated your DSCR. You pulled the rent, divided by the mortgage payment, and the number looked fine. Most investors do exactly this, and most investors get a different number than the lender does.

That gap isn’t a rounding error. It’s a fundamentally different set of assumptions — about what counts as income, what counts as expense, and how much cushion the lender needs before they’ll put capital behind your deal. Most DSCR calculators online assume perfect rents and perfect expenses. Lenders don’t. They assume risk. They assume vacancy. They assume the version of your deal that survives a bad quarter.

This page isn’t a calculator. It’s the logic behind the calculation — the way lenders actually build the number, and the specific places where your math and their math diverge. Understanding this before you submit a deal is the difference between a smooth close and a renegotiation you didn’t see coming.

Why Most DSCR Calculations Are Wrong

The formula itself is simple. Rental income divided by total debt service. Investors know this. The problem isn’t the formula — it’s what you plug into it.

Pro forma rent vs. in-place rent

Investors routinely calculate DSCR using projected rent — what they believe the property will earn once they stabilize it, raise rents to market, or convert to short-term rental. Lenders don’t underwrite projections. They underwrite what’s documented. If there’s an existing lease, the lender uses the lease amount or the appraiser’s market rent opinion, whichever is lower. If the property is vacant, they use the appraiser’s rent schedule — which is almost always more conservative than the investor’s estimate. The number you’re excited about and the number the lender uses are frequently not the same number.

Expense underestimation

Most investor-side DSCR calculations account for principal, interest, taxes, and insurance. Some include HOA. Almost none include the full expense load that lenders apply. Property management fees get included even if you self-manage — because the lender is underwriting the deal, not your lifestyle. Maintenance reserves, flood insurance in applicable zones, and special assessments can all appear on the lender’s side of the calculation that didn’t appear on yours. Each one compresses the ratio.

Vacancy assumptions

An investor with a signed lease calculates DSCR at 100% occupancy. The lender applies a vacancy and collection loss factor — typically 5–10% depending on the market and property type — because leases end, tenants default, and turnover costs money. On a deal where the DSCR is 1.20 at full occupancy, a 7% vacancy haircut drops it to roughly 1.12. That’s a meaningful shift, and in some cases it moves the deal below a lender’s minimum threshold.

Interest-only vs. fully amortized confusion

This catches more experienced investors than you’d expect. If you’re quoting a DSCR based on an interest-only payment but the lender is qualifying the deal on a fully amortized basis — or vice versa — you’re working with two completely different ratios. Some lenders qualify at the IO payment during the IO period. Others qualify at the fully amortized payment regardless of structure. If you don’t know which method your lender uses, your DSCR is a guess.

How Lenders Calculate DSCR (Step by Step)

Lender DSCR calculation follows a specific logic. It’s not complicated, but every step involves a judgment call that can move the number. Here’s the actual sequence.

Step 1: Establish gross rental income

The lender starts with the property’s income. For long-term rentals, this is the lesser of the in-place lease amount and the appraiser’s fair market rent opinion from the 1007 rent schedule. If the property is vacant, they rely entirely on the appraiser’s estimate. For short-term rentals, income documentation requirements vary significantly — some lenders accept 12 months of booking history, others use third-party projections, and some won’t underwrite STR income at all. The income figure the lender establishes at this step is the ceiling for everything that follows.

Step 2: Apply vacancy and collection loss

The lender reduces gross income by a vacancy factor. This is typically 5–10% but can be higher in markets with elevated vacancy rates or for property types with higher turnover. This isn’t negotiable — it’s baked into the underwriting model. Your actual occupancy history might be 98%, but the lender is pricing in the statistical reality that vacancy happens.

Step 3: Determine effective rental income

After the vacancy haircut, you have the effective rental income — the number the lender treats as the property’s actual earning capacity. Some lenders make additional adjustments here for property management fees or maintenance reserves, further reducing the income figure before it enters the ratio calculation.

Step 4: Calculate total debt service (PITIA)

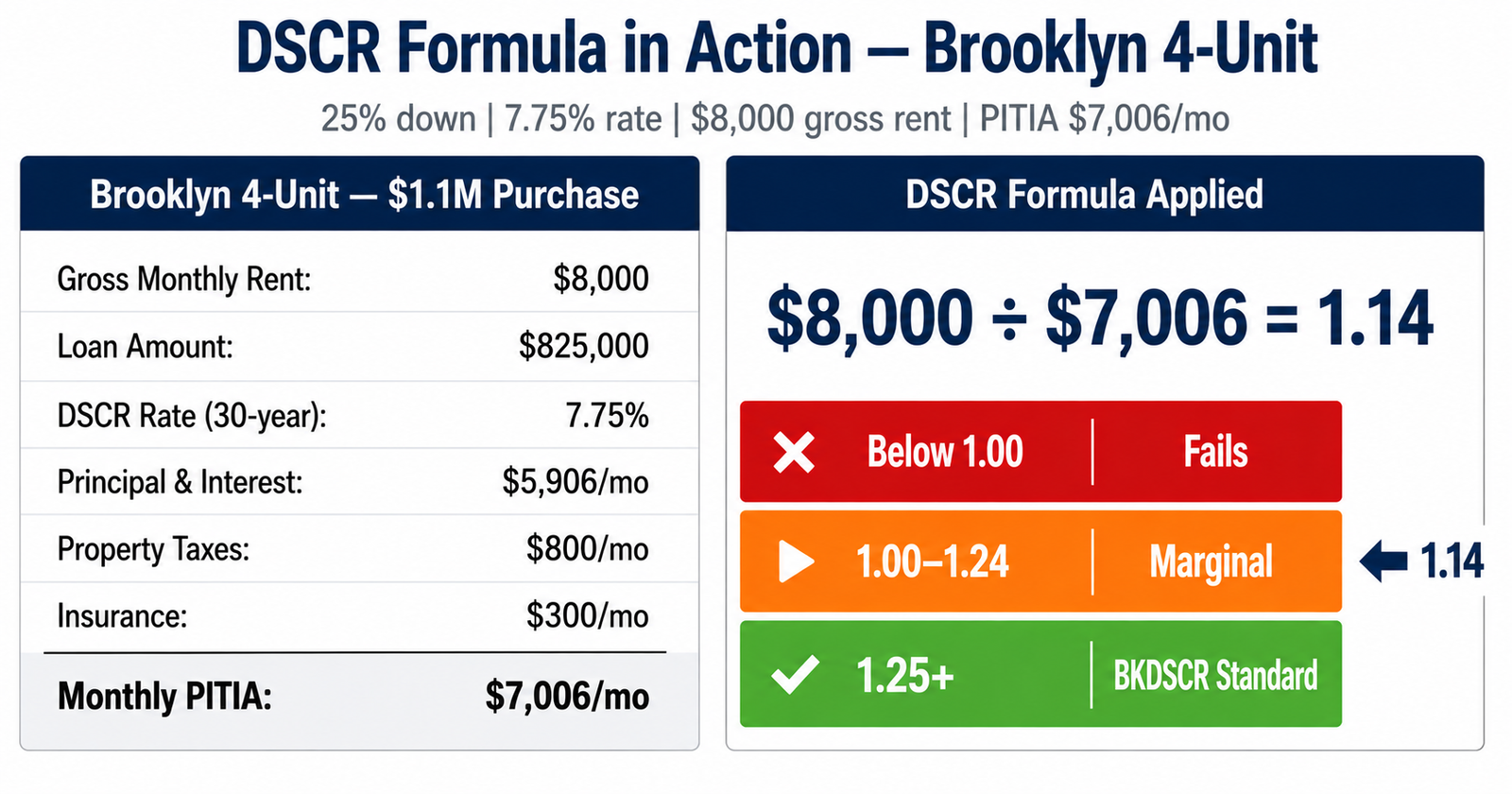

This is where the denominator gets built. Total debt service in DSCR lending is not just principal and interest. It’s PITIA: principal, interest, taxes, insurance, and association dues. Every component of the monthly housing obligation gets included. If there’s flood insurance, it’s in. If there’s an HOA or condo fee, it’s in. Property taxes are the most commonly underestimated component of PITIA. NYC property tax rates from the NYC Department of Finance can add $600–$1,200 per month to PITIA on a typical outer-borough 4-unit deal — a difference large enough to move the DSCR ratio by 0.10–0.15 points. The lender calculates this using the actual loan terms — but as noted above, some lenders qualify at the fully amortized payment even during an IO period.

Step 5: Divide and evaluate

Effective rental income divided by total debt service equals the lender’s DSCR. This is the number that determines whether your deal clears the threshold, what pricing tier you land in, and whether additional conditions get attached. A ratio of 1.00 means the property exactly covers its debt. Most lenders require a minimum above 1.00 — typically 1.10 to 1.25 depending on the lender, the property type, and the borrower’s profile.

DSCR Thresholds That Actually Matter

Not all DSCRs are equal. The number itself determines more than just approval or denial — it determines your rate, your LTV, your reserve requirements, and in some cases whether the lender will even look at the file. Here’s how the thresholds actually function.

1.00x — Breakeven

A DSCR of 1.00 means the property’s income exactly covers its debt service with zero margin. Some lenders will fund at 1.00, but the terms reflect the risk: lower LTV, higher rate, larger reserve requirements, and often restrictions on property type. A 1.00 deal isn’t necessarily bad — it may cash flow positively once you factor in tax benefits, appreciation, and principal paydown. But from the lender’s perspective, there’s no income cushion. Any rent reduction, vacancy event, or expense increase puts the loan underwater on a cash flow basis.

1.10x–1.15x — Minimum viable

This is where most DSCR lenders set their practical floor for competitive terms. A 1.10–1.15 ratio gives the lender a modest margin of safety and typically unlocks standard pricing. But “standard” doesn’t mean “best.” Deals in this range are often priced at higher rates than deals at 1.20 or above, and the lender may apply additional conditions — lower maximum LTV, higher reserve requirements, or restrictions on loan structure.

1.20x–1.25x — The sweet spot

Most lenders price most favorably in this range. A 1.20–1.25 DSCR indicates the property generates 20–25% more income than it needs to cover its debt. That cushion absorbs vacancy, expense increases, and minor rent softening without putting the loan at risk. Deals in this range typically qualify for the best rates, highest LTV options, and most flexible terms. If you’re structuring a deal and have room to optimize — through rent improvements, expense reductions, or rate adjustments — getting above 1.20 often has a disproportionate impact on your total cost of capital.

1.30x+ — Diminishing returns

Above 1.30, most lenders aren’t offering significantly better terms. The pricing improvement flattens. If your deal naturally sits here, that’s a strong position — but engineering a DSCR above 1.30 by overpaying in points or making structural concessions usually isn’t worth the marginal improvement in terms.

How property type shifts the threshold

The same DSCR doesn’t carry the same weight across all property types. A 1.15 on a stabilized duplex in a strong rental market is a different risk profile than a 1.15 on a condotel or a rural single-family with one lease. Lenders adjust their minimum thresholds by property type, and some property categories require ratios of 1.25 or higher just to qualify. Your target DSCR shouldn’t be a fixed number — it should reflect what the specific lender requires for the specific property type you’re financing.

Edge Cases Investors Miss

Standard DSCR calculations work cleanly when you have a stabilized long-term rental with a fixed-rate loan and a signed lease. The moment any of those variables changes, the calculation gets more nuanced — and the gap between your number and the lender’s number widens.

Short-term rental underwriting

STR income is inherently variable, and lenders treat it that way. Some require 12–24 months of documented booking history and use the trailing average as income. Others accept third-party projections from platforms like AirDNA but apply a discount of 10–25%. A few won’t underwrite STR income at all and will only use long-term comparable rents. If your deal’s DSCR depends on STR-level income, the specific lender’s STR underwriting policy is the single most important variable in your approval. Two lenders looking at the same property can produce DSCRs that are 30–40 basis points apart based purely on how they treat the income.

Seasonal rent variation

Properties in seasonal markets — beach towns, ski areas, college towns — have income that fluctuates significantly by month. A property that grosses $4,000 per month in summer and $1,500 in winter has an average that looks fine. But lenders may not average smoothly. Some weight recent months more heavily. Others look at the lowest-performing quarter as a stress indicator. If your annualized rent looks strong but your off-season income barely covers the mortgage, expect the lender to flag it.

Multi-unit rent averaging

On multi-unit properties, the DSCR is typically calculated on aggregate income versus aggregate debt service. But how the appraiser assigns rent to individual units matters. If one unit in a fourplex is below market and the appraiser uses in-place rents across the board rather than market rents, your aggregate income — and therefore your DSCR — takes a hit disproportionate to the one underperforming unit. Investors who assume appraisers will use market rent on vacant or below-market units are frequently disappointed.

Rate lock timing

Your DSCR is a function of your debt service, and your debt service is a function of your rate. If you calculate DSCR before locking a rate and rates move against you between application and lock, your DSCR changes — sometimes significantly. A 25-basis-point rate increase on a $500,000 loan at 30-year amortization adds roughly $80–$90 per month to debt service. On a deal with a tight ratio, that movement can drop you below threshold. The DSCR you calculated at the time of application is not the DSCR you close with unless the rate is locked.

Renovation and stabilization timing

BRRRR investors and value-add operators often calculate their “after” DSCR based on projected stabilized rent post-renovation. But most DSCR lenders underwrite current income, not projected income. If the property isn’t stabilized at the time of application — units are still being turned, rents haven’t been seasoned, or the renovation isn’t complete — the lender’s DSCR will reflect the property’s current state, not your business plan. This is a sequencing issue: the deal needs to be stabilized before DSCR financing fits, and investors who apply too early burn time and sometimes earnest money.

What to Review Before Trusting Your DSCR

A DSCR number is only as reliable as the assumptions underneath it. Before you treat any calculation as a green light, pressure-test it against the reality of how lenders will evaluate the deal.

Are you using the appraiser’s rent estimate or your own? If you’re using yours, expect a correction. Calculate with the lower number and see if the deal still works.

Does your calculation include a vacancy factor? If not, reduce gross income by at least 5–7% and recalculate. If the deal only works at 100% occupancy, it doesn’t work.

Is your debt service PITIA — or just P&I? Taxes, insurance, HOA, and flood insurance all belong in the denominator. Leaving any of them out inflates your ratio.

Are you calculating at the IO payment or the fully amortized payment? Know which one your lender uses for qualification, and calculate both so you understand your range.

Is your rate locked? If not, stress-test the DSCR at 25–50 basis points above your quoted rate. If the deal doesn’t survive that movement, your approval is rate-dependent — and rate-dependent approvals fail.

Does the lender underwrite your property type and income source the way you’re modeling it? STR income, seasonal rent, and multi-unit averaging are all treated differently across lenders. If you haven’t confirmed this, your calculation may be based on assumptions the lender doesn’t share.

If any of those answers reveal a gap between your number and the lender’s likely number, close it before you submit. One more piece gets missed all the time: the loan structure itself.

Prepayment Penalty Selector

DSCR math tells you whether the deal qualifies. Prepayment structure tells you whether you can exit without getting hit. Match the penalty to your likely hold period before you submit.

Simple rule: don’t choose the lowest rate first. Choose the structure that matches your exit.

DSCR Lender Criteria →

Understand the specific underwriting requirements, overlays, and property-type restrictions that lenders apply beyond the ratio itself. The DSCR gets you in the door. The criteria determine what happens inside.

DSCR Deal Analysis Framework →

Walk through the complete deal evaluation process — from rent validation and expense verification through stress testing and structural term analysis — the way a lender would before you submit.

Or get the full picture in one document

the calculator logic, the lender adjustments, and every assumption that moves your number.

Already working a deal?

No Hype. Just Real Numbers.