DSCR Deal Killers — The 7 Reasons NYC Rental Deals Fail Underwriting

Why “Good” Deals Get Rejected

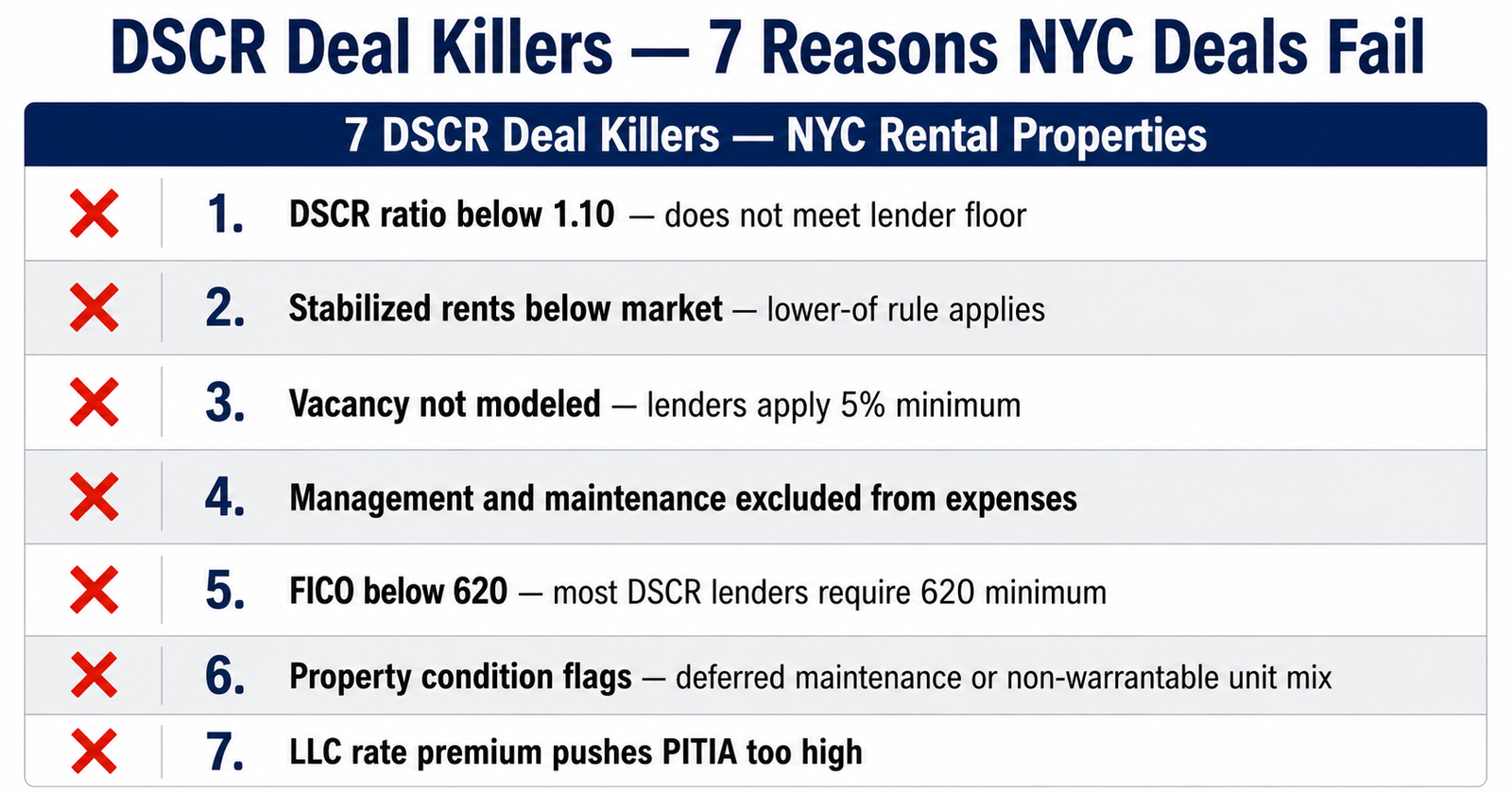

Deal Killer #1 — DSCR Ratio Too Low to Qualify

Most DSCR rejections aren’t about the ratio. They’re about risk the ratio doesn’t capture. An investor submits a deal with a 1.20 DSCR, solid credit, and clean documentation. The deal gets conditioned, repriced, or declined. Not because the numbers are wrong, but because something underneath the numbers — the income assumptions, the expense exposure, the market trajectory, or the structural fit — triggers a risk flag the investor didn’t see coming.

These are deal killers. They operate below the ratio, outside the rate sheet, and beyond what most DSCR content ever covers. They’re the reason experienced investors with strong portfolios still get surprised. And they’re almost always identifiable before submission — if you know where to look.

This page maps every major category of DSCR deal killer: income, expense, property, market, and structure. Each one includes the specific scenario that triggers rejection and the logic behind the lender’s decision. The goal isn’t to scare you out of deals. It’s to make sure you kill bad deals yourself — before the lender does it for you, on their timeline, at your cost.

Unlike conventional financing, DSCR loans do not use debt-to-income ratio standards from the CFPB's borrower qualification framework — they replace DTI with the property's own income-to-debt ratio. Understanding that distinction explains why deals that pass conventional DTI tests can still fail DSCR underwriting.

Deal Killer #2 — Rental Income That Lenders Will Not Count

Income is the numerator of the DSCR equation, and it’s where the most consequential gaps between investor expectations and lender calculations occur. Every dollar of income the lender discounts compresses the ratio. When the income assumption is the foundation of the deal, even a modest correction can be fatal.

Inflated rent expectations

The investor models rent based on what they believe the property can achieve — pro forma rent, aspirational comps, or renovation-adjusted projections. The lender uses the lesser of the in-place lease and the appraiser’s rent schedule. If the investor’s number is $2,400 and the appraiser’s number is $2,050, the DSCR drops by 15%. On a deal with a thin margin, that correction is the difference between funded and declined.

This is the single most common income-related deal killer, and it’s the most preventable — because the investor can pull comps and estimate the appraiser’s range before submitting.

Unverifiable income

Lenders require documented income. For long-term rentals, that means a signed lease or the appraiser’s market rent opinion. For short-term rentals, it means 12–24 months of booking history, platform income statements, or third-party projections from approved sources.

Verbal representations, handshake agreements, cash payments without documentation, and projected income from a property that hasn’t been rented yet don’t qualify. If the income can’t be verified through documentation the lender accepts, the income doesn’t exist for underwriting purposes.

STR income assumptions

Short-term rental projections are the highest-variance income source in DSCR lending. An investor looking at peak-season Airbnb data or optimistic projections may see annual income that supports a strong DSCR. The lender applies occupancy discounts, seasonal adjustments, and sometimes a blanket income reduction.

Two lenders evaluating the same STR property can arrive at income figures 20–35% apart. If the deal only works at the investor’s STR projection and not at the lender’s adjusted figure, the deal is built on an assumption the lender won’t accept.

Seasonal volatility

Properties in seasonal markets generate income unevenly. A beach rental that grosses $5,000 per month in summer and $1,200 in winter has an annual average that may look adequate. But lenders evaluate income durability, not just averages.

If the off-season income doesn’t cover the monthly debt service, the lender sees a property that’s cash-flow negative for four to five months per year. Some lenders average across the year. Others weight the low-income months more heavily. And some apply a higher DSCR minimum to account for the volatility.

Seasonal properties need to be underwritten as seasonal properties — not as annualized averages.

The income the lender uses is the income the lender can defend. If your deal depends on an income assumption the lender can’t verify, document, or stress-test, the deal is already at risk.

Expense Blind Spots

Income gets the attention. Expenses kill the deal. The denominator of the DSCR equation — the total debt service and carrying costs — is where lenders apply assumptions that investors routinely underestimate or miss entirely.

Underestimated property taxes

Investors often use current tax amounts in their DSCR calculation. The problem: property taxes in many jurisdictions are based on the last assessed value, which may be years old or reflect a homestead exemption that doesn’t apply to investment property.

Upon sale, the property gets reassessed at the purchase price — and the tax bill jumps. In some markets, this reassessment can increase annual taxes by 30–60%. The lender anticipates this. They’ll use the estimated post-purchase tax amount, not the current bill. If your DSCR math uses today’s taxes on a property you’re about to buy, your denominator is too small.

Insurance shock

Property insurance markets in coastal, storm-prone, and wildfire-exposed areas have experienced major premium increases, with some areas losing carrier availability entirely.

An investor who quotes insurance from a year ago or uses a rough estimate may find the actual binding quote at closing is significantly higher. The lender uses the actual insurance cost — and if the premium comes in higher than projected, the DSCR drops at the worst possible time: during final underwriting. In extreme cases, the investor can’t obtain coverage at any reasonable price, and the deal dies on insurance alone.

HOA restrictions and special assessments

HOA dues are a known expense. What investors miss are the restrictions and hidden costs within the HOA. Rental restrictions can affect income assumptions and lender eligibility. Special assessments can add thousands to annual carrying costs.

Some HOA governing documents also contain provisions that conflict with lender requirements, making the property ineligible regardless of the numbers.

Deferred maintenance

DSCR loans require the property to be in rent-ready condition. Deferred maintenance that shows up in the appraisal — roof at end of life, foundation issues, outdated electrical, plumbing deficiencies, or active water damage — can trigger required repairs, a reduced appraised value, or outright declination.

The lender isn’t evaluating what the property could be after repairs. They’re evaluating what it is today. If it doesn’t meet their condition standards, the deal stops until it does.

Expenses are facts, not estimates. Every expense the lender verifies and you didn’t account for compresses your ratio by an amount you didn’t model. The deal killer isn’t the expense itself. It’s the gap between what you planned for and what showed up.

DSCR Red Flags NYC Lenders Flag at Underwriting

A deal can have solid income, controlled expenses, and a clean DSCR — and still fail because the property or the market carries risk the lender won’t absorb. These aren’t calculation problems. They’re eligibility problems.

Rural and low-population markets

Many lenders price risk partly based on liquidity: how quickly could they sell the property if the borrower defaults? Properties in rural areas or small towns carry higher disposition risk.

Many lenders apply reduced LTV caps, higher DSCR minimums, or outright geographic exclusions for markets below certain population thresholds. A strong deal in a town of 15,000 may simply be outside most lender boxes — not because the numbers are wrong, but because the market doesn’t support the lender’s exit.

Declining zip codes

Markets with falling values, rising vacancy, population loss, or employer contraction are treated differently than stable or growing markets. Some lenders use market scoring models; others rely on underwriter discretion.

Either way, a property in a declining market faces headwinds that a strong DSCR alone can’t overcome. The lender is making a bet that lasts years. If market trajectory suggests the property will be worth less and earn less in five years, today’s ratio becomes less persuasive.

Unique and non-standard assets

Non-standard construction, conversions, live-work configurations, leased land, and deed-restricted assets create underwriting problems most DSCR lenders aren’t equipped to handle.

These properties may cash-flow, but they’re harder to comp, harder to sell, and harder to predict. Unique assets require specialized lenders — a smaller pool with different terms.

Liquidity and marketability issues

Condo buildings with high investor concentration can be non-warrantable. Properties with litigation, title clouds, or environmental issues create legal risk lenders won’t accept. Some properties face valuation haircuts if the realistic buyer pool is investors only.

If the lender can’t confidently project disposition value, they price that uncertainty into the terms — or they decline.

Lenders don’t just evaluate whether the deal works today. They evaluate whether they can exit the deal if it stops working. Property and market risk drive that assessment — and no ratio makes a bad market or an illiquid asset acceptable.

Structural Deal Killers

Structural deal killers are the most frustrating category because they’re not about the quality of the deal. They’re about the fit between the deal and the specific loan product.

Loan size below minimum

Most DSCR lenders have minimum loan amounts. A strong deal in a lower-cost market can produce a loan amount below the threshold, especially at conservative LTV levels.

This is purely mechanical. The deal can be perfect in every other dimension and still be unfundable because the dollar amount doesn’t meet the lender’s operational minimum.

LTV stacking and leverage limits

Creative capital stacking (second liens, seller concessions, subordinate debt) can push total leverage beyond lender limits. DSCR lenders have strict policies on subordinate financing and combined LTV.

A deal structured with a DSCR first lien at 75% LTV plus a second lien pushing total leverage to 90% will be declined by most lenders if discovered. These policies interact with liquidity requirements and borrower net worth expectations.

IO misalignment

A structure built around interest-only payments may not align with the hold period, the rate type, and the exit timeline. A 3-year IO period on a 7-year hold creates a payment cliff.

If post-IO cash flow doesn’t support debt service, the investor faces an early refi (often inside the prepay window) or a cash-flow-negative hold. The structure works briefly — then falls apart.

Exit risk and prepayment traps

Every DSCR loan has an exit. The question is whether the exit is planned or forced — and whether it’s affordable. A 5-4-3-2-1 prepay on a $400,000 loan can mean a $20,000 penalty in year one, $16,000 in year two, and so on.

If that cost isn’t modeled, the deal’s real yield is lower than projected. Worse: if rates move and the refi DSCR doesn’t qualify, the investor can be trapped through the penalty period. The killer isn’t the prepay itself. It’s the mismatch between prepay terms and actual strategy.

Structural deal killers are the most avoidable. Every one of them is disclosed before closing. They become deal killers when the investor doesn’t model them against strategy — or chooses the lender before choosing the structure.

Screen Before Wasting Time

Every DSCR Deal Killers on this page is identifiable before submission. The income gap, the expense blind spot, the property-level disqualifier, the market flag, the structural mismatch — none of them require underwriting to discover. They require the investor to look at the deal the way the lender will, in the order the lender does, against the criteria the lender actually applies.

Most investors don’t do this. Not because they don’t care, but because mapping a specific deal against a specific lender’s criteria, overlays, and structural parameters takes more effort than most investors have time for on every deal. The result is reactive discovery: the deal killer surfaces during underwriting, the investor scrambles to restructure or find an alternative lender, and time and money get burned.

The alternative is screening the deal before you commit to it.

Screen Your Deal with the 60-Second DSCR Deal Filter →

The deal filter checks your deal against every category on this page — income validation, expense verification, property and market eligibility, and structural fit — before you invest time in a lender submission. If there’s a deal killer, you’ll see it before the lender does. If the deal is clean, you’ll know that too. No email required. No sales pitch. Just a clear read on your deal.

Or get every DSCR Deal Killers mapped out in one document — plus the math, the lender criteria, and the structural fixes

The full scope.

Already working a deal?

No Hype. Just Real Numbers.

BKDSCR is an independent DSCR education and advisory platform. We do not originate loans or act as a mortgage broker. BKDSCR may receive compensation from partner lenders when a client introduction results in a closed loan. This does not affect the independence of our analysis or deal review process.