DSCR is just one input. Most investors treat it like the finish line — hit the ratio, get the loan. In practice, the ratio is closer to the starting gate.

What determines whether your deal actually closes, what terms you get, and how long it takes is a layer of criteria that most borrowers never see until it stops them.

Lender criteria operate on three levels: property, borrower, and deal structure. Each level has published guidelines and unpublished overlays. The published guidelines tell you what’s theoretically possible. The overlays tell you what actually happens when a real deal hits the underwriting desk.

This page maps the full criteria landscape. Not theory. Not generalizations. The specific factors that move deals from submission to approval or from submission to dead file.

Property-Level Criteria

Before a lender evaluates your numbers, they evaluate the asset. Property-level criteria are the first filter — and for many investors, the most surprising source of deal failure. A strong DSCR on a property the lender won’t touch is a wasted underwriting cycle.

Property types: what’s in and what’s out

Most DSCR lenders fund single-family homes, 2–4 unit properties, condos (warrantable), and townhomes without issue. Beyond that, it gets selective.

Non-warrantable condos, condotels, mixed-use properties with commercial components, manufactured housing on permanent foundations, and properties with acreage above certain thresholds all carry restrictions that vary by lender.

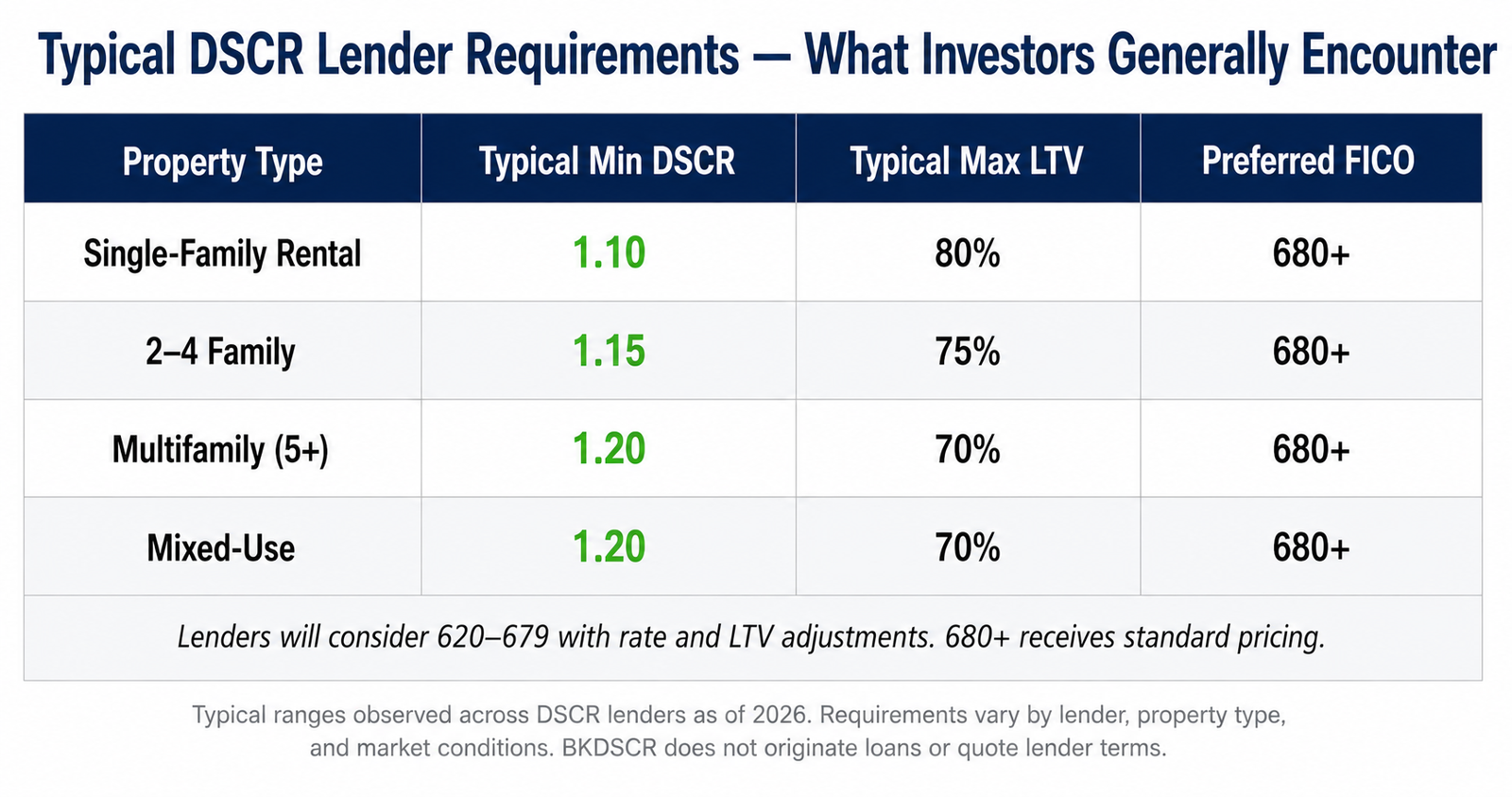

Some lenders fund 5–10 unit properties under their DSCR program. Others cap at four. The property type isn’t just a checkbox — it determines which lenders are even in play, what rate tier you’re in, and what minimum DSCR applies.

Condition requirements

DSCR loans are not rehab loans. Lenders expect the property to be habitable, rent-ready, and free of material deferred maintenance at closing.

Peeling paint, structural issues, roof at end of life, active code violations, or environmental hazards will stall or kill the deal. Some lenders require a minimum condition rating from the appraiser. Others rely on appraisal photos and interior inspection.

If the property needs work to reach rent-ready condition, the sequencing matters: rehab first with appropriate financing, stabilize, then come to DSCR lending.

Geographic overlays

Not every lender lends everywhere, and lenders who do lend nationally don’t treat every market equally. Geographic overlays are among the least visible criteria — they’re rarely published in rate sheets — but they’re aggressively applied.

Markets with declining populations, elevated vacancy rates, economic concentration risk, or natural disaster exposure often trigger reduced LTV caps, higher DSCR minimums, or outright declinations.

Coastal flood zones, wildfire-prone areas, and markets with recent insurance market disruptions carry additional scrutiny. Confirm lender appetite for your specific geography before running numbers.

Short-term rental restrictions

STR eligibility is one of the most inconsistent criteria across DSCR lenders. Some lenders welcome STR income and have dedicated underwriting tracks for it.

Others accept it with heavy documentation requirements — typically 12–24 months of booking history, third-party income projections, and sometimes a separate STR-specific appraisal.

Many lenders won’t underwrite STR income at all and will only use long-term comparable rents for the DSCR calculation. If your deal depends on STR income, the lender’s STR policy is a threshold question.

Property-level criteria are binary. Either the lender funds that property type in that market under those conditions, or they don’t. No amount of borrower strength or deal structure optimization overrides a property that falls outside the lender’s box.

Borrower Criteria (Lighter Than Conventional — But Real)

DSCR lending is property-focused, but it’s not borrower-blind. Lenders evaluate the person (or entity) behind the deal — just through a different lens than conventional lending.

Credit bands

Credit score is the single largest borrower-level pricing factor in DSCR lending. Most lenders have a hard floor — typically 660–680, with some expanded programs down to 620 at higher rates.

Above the floor, pricing improves in bands (680–700, 700–720, 720–740, 740+). The spread between a 680 and a 740 can be 75–150 basis points or more depending on the lender.

Credit optimization before applying isn’t vanity — it’s a cost-of-capital decision.

Liquidity and reserves

Lenders want to see you can absorb vacancy, unexpected expenses, or a temporary income disruption without defaulting. Reserve requirements often range from 6 to 12 months of PITIA.

What counts as “liquid” varies: some lenders count retirement accounts at a discounted value; others only count cash and securities. Published minimums of 6 months frequently become 9 or 12 months for certain deal profiles.

Experience

Some DSCR lenders have no experience requirement. Others require a minimum number of investment properties owned or transactions completed in a defined period.

First-time investors aren’t locked out, but the lender pool is smaller, terms are less favorable, and reserve requirements are typically higher.

Entity structuring

Most DSCR lenders allow closing in an LLC. Some also accommodate land trusts, revocable living trusts, and S-corps. Recently formed entities are generally fine — lenders aren’t looking for operating history on the LLC.

What they are looking for is clean structure: the entity owns the property, the guarantor controls the entity, and the operating agreement doesn’t contain provisions that conflict with lender requirements.

The borrower criteria in DSCR lending aren’t designed to verify your income. They’re designed to verify that you can survive a disruption. If the property goes vacant for three months, does this borrower have the resources and track record to weather it?

Deal Structure Criteria

Once the property clears and the borrower qualifies, the conversation shifts to structure. This is where terms get built — and where the interplay between LTV, rate, structure, and DSCR creates the real economics.

LTV caps

Maximum LTVs typically range from 70–80% depending on lender, property type, DSCR, and credit score. Cash-out refinances usually carry lower max LTVs than purchases.

STR properties, non-warrantable condos, and higher-risk markets frequently have reduced LTV caps. The LTV you see in marketing is the ceiling. The LTV you receive is a function of the full profile.

Rate structure: fixed vs. adjustable

DSCR loans come as fixed-rate and ARMs (often 5/6, 7/6, 10/6). The spread between fixed and adjustable can be 50–100+ basis points — and can change whether the deal qualifies.

Interest-only eligibility

IO periods of 1–5 years are available from many DSCR lenders, but eligibility isn’t automatic. Lenders typically restrict IO to higher credit scores, lower LTVs, and stronger DSCRs.

IO also interacts with qualification: some lenders calculate DSCR using the IO payment; others use the fully amortized payment regardless. If you’re counting on IO to push DSCR above threshold, confirm how the lender qualifies before you submit.

Consumer Financial Protection Bureau (CFPB) — .gov

DSCR loans are classified as non-QM products — they sit outside Fannie Mae and Freddie Mac guidelines. The CFPB explains non-QM loan guidelines and what distinguishes them from conventional qualifying rules, which is the framework most DSCR lenders operate within.

Prepayment penalties

Nearly all DSCR loans carry prepayment penalties. Common structures include stepdowns (5-4-3-2-1 or 3-2-1), yield maintenance, and defeasance on larger loans.

The penalty structure affects your exit flexibility. Structure your deal for the exit, not just the entry.

Prepayment Penalty Selector

Most investors focus on rate. Lenders price structure. Match the penalty to your likely exit before you submit.

Rule: short-term exits need flexibility. Medium holds usually fit 3-2-1. True long-term holds can justify 5-4-3-2-1.

Rate is the number investors negotiate hardest. Prepay penalty is the number that costs them the most when the strategy changes. Structure your deal for the exit, not just the entry.

Common Lender Overlays

Overlays are stricter-than-published criteria lenders apply based on risk appetite, market conditions, portfolio composition, and underwriter discretion. They’re not on the website. They’re not in the rate sheet. And they’re why clean-looking deals get conditioned, repriced, or declined.

Market risk overlays

A property in a lender’s “high risk” market can face LTV reductions, higher DSCR minimums, or rate adjustments — and those overlays can change without notice.

DSCR stress test overlays

Some lenders run stress scenarios that can turn an apparent approval into a conditional approval or a decline. Deals near the minimum DSCR are most vulnerable.

Minimum loan size

Most DSCR lenders have minimum loan amounts (often $75k–$150k+). Below the minimum, the deal won’t be funded regardless of strength.

Rent source exclusions

Voucher income, corporate housing, rent-by-the-room, student housing, and related-party tenants can trigger restrictions. If your rent isn’t standard long-term third-party lease income, confirm policy early.

Concurrent loan limits

Some lenders cap total DSCR loans per borrower/guarantor (5, 10, 20 are common). It’s a portfolio-level policy — unrelated to your current deal quality.

Overlays exist because lenders price risk that doesn’t show up in the ratio. Your DSCR tells them about the deal. Overlays tell them about everything the deal doesn’t say.

Before You Submit a Deal

The investors who close DSCR deals without surprises aren’t working with better lenders. They’re matching the deal to the lender’s criteria before submission — not hoping the criteria match after.

Every variable on this page is knowable in advance: property type eligibility, geographic restrictions, credit band pricing, LTV caps, reserve requirements, STR policy, prepay structure, overlay exposure — all of it can be confirmed before you invest time, money, and momentum into a file that doesn’t fit.

Does the lender fund this property type in this market? Confirm eligibility for your specific property category and geography before anything else. This is a binary gate — nothing downstream matters if the answer is no.

What credit band are you in, and what does that cost? Know your score, know the lender’s pricing tiers, and calculate the rate impact.

Do your reserves meet the lender’s actual requirement? Not the published minimum — the requirement for your specific deal profile.

Is your loan structure aligned with your investment timeline? IO period, rate type, and prepay penalty should match your hold period and exit strategy.

Have you identified overlays that apply? Market classification, stress test methodology, concurrent loan limits, and rent source restrictions are knowable — they’re just not volunteered.

If you want to screen a deal against lender criteria before submitting it — to identify gaps, overlay exposure, and structural mismatches before they cost you time — run it through the 60-Second DSCR Deal Filter.

Or get the full scope in one document

Lender criteria, deal structure, calculator logic, and the screening framework — all in one document.

Already working a deal?

No Hype. Just Real Numbers.