DSCR Deal Qualification NYC — Before You Submit, Run the Numbers

A simple way to know “yes”, “no”, or “not yet” before you submit

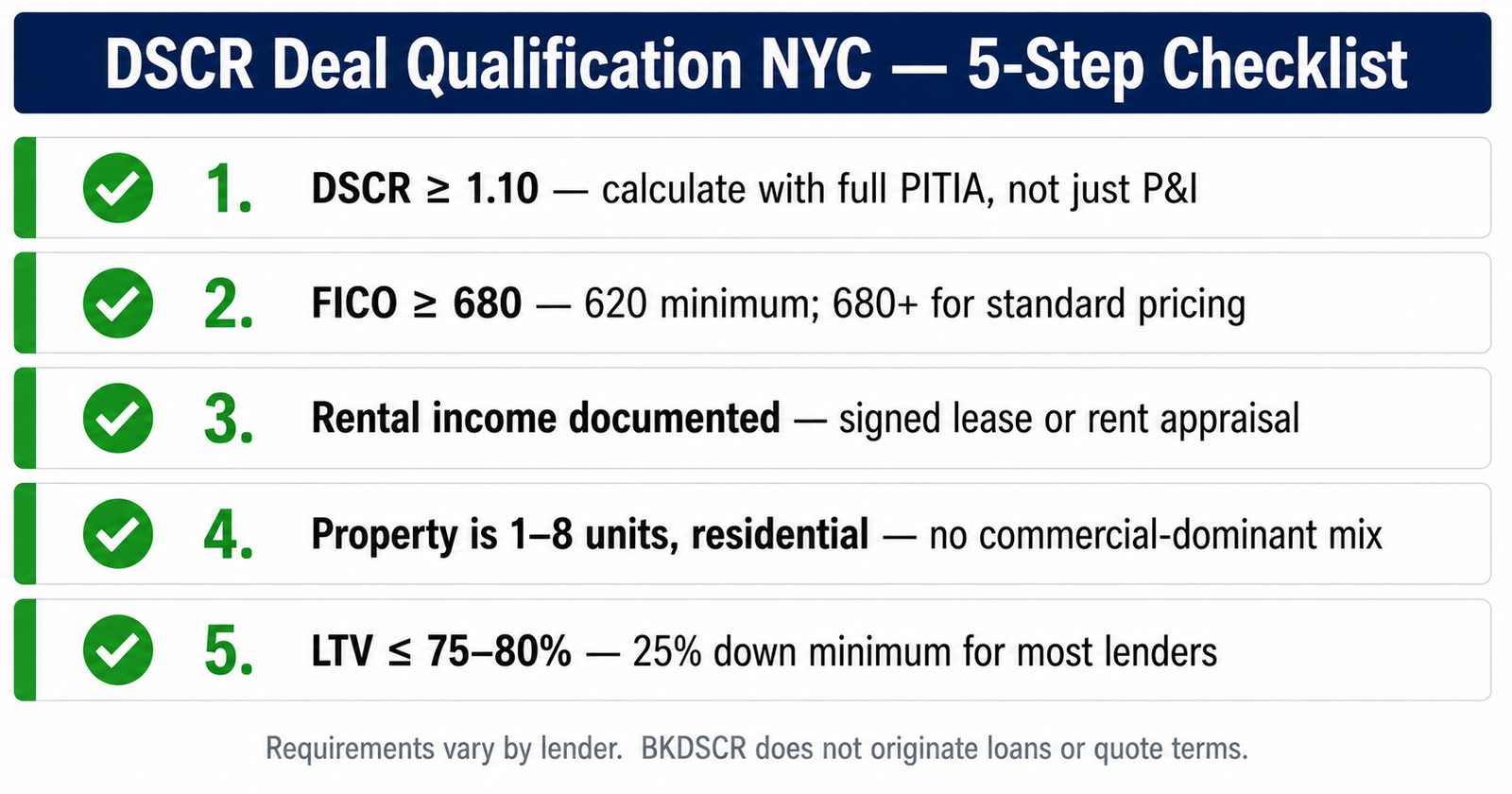

What DSCR Deal Qualification NYC Actually Requires

Most investors ask the wrong question first: “What’s the DSCR?”. The real question is: “Will a lender accept this deal under DSCR loan guidelines — with the inputs the lender uses, not the inputs I wish they used?”

Qualification is not one number. It’s a sequence. If you fail early in the sequence (property type, market, documentation, structure), the DSCR ratio doesn’t matter. This page gives you a fast, lender-style filter — so you know where the deal stands before you burn time.

DSCR loan qualification operates outside the Fannie Mae investor lending guidelines that govern conventional investment property financing — which is why investors who cannot clear conventional DTI limits or the 10-property cap often qualify on DSCR instead.

DSCR Loan Qualification Checklist — 5 Things to Confirm First

Gate 1: The property is eligible

- Property type: SFR/2–4 is usually straightforward; condos, mixed-use, condotels, 5–10 units, rural, and STRs vary by lender.

- Condition: DSCR loans are not rehab loans. If it’s not rent-ready, you’re likely “not yet.”

- Market appetite: Some zip codes get overlays (lower LTV, higher DSCR minimums, or no go). See Lender Criteria.

Gate 2: The income is underwritable

- Rent source: long-term lease vs projected rent vs STR history. Lenders usually cap income at the most defensible source.

- Vacancy factor: lenders haircut rent. If your deal only works at 100% occupancy, it’s fragile.

- Reality check: learn how lenders build the ratio on the DSCR Formula page.

Gate 3: The structure fits the lender box

- LTV: leverage changes the payment, which changes DSCR. Tight ratios + max leverage is where deals die.

- Rate + payment type: some lenders qualify on amortized payments even if the loan is interest-only.

- Prepay terms: your strategy has to match the penalty. If not, the exit becomes expensive.

Gate 4: Borrower profile clears minimums

- Credit: the biggest pricing lever, and sometimes a hard gate.

- Reserves: lenders want to know you can survive vacancy and repairs.

- Entity: most lenders allow LLCs, but structure must be clean.

Gate 5: The deal survives stress

- Rate moves: small changes can push a borderline DSCR below threshold. Use the DSCR Stress Test.

- Expense creep: insurance, taxes, HOA, and repairs compress your cushion.

- Refi exit: many “good deals” break at refinance. Run the exit scenario on the Refi Analyzer.

How to Qualify for a DSCR Loan — What Investors Get Wrong

Likely “Yes”

The property is standard (SFR/2–4), rent is documented, the DSCR is comfortably above the lender’s minimum, and the deal still works when you stress it.

Likely “No”

The property is ineligible for most lenders, the income can’t be documented the way the lender requires, the DSCR is below minimum after lender adjustments, or the structure (LTV/payment/prepay) doesn’t match lender rules.

Likely “Not Yet”

The deal might work, but it needs sequencing: finish the rehab, stabilize rent, season STR income, bring reserves into place, or reduce leverage.

Use These Two Pages in Order

1) Read Deal Killers →

If your deal has a hidden failure point, it’s usually one of these. This is the “why deals die” checklist.

2) Run the 60-Second Deal Filter →

Quick scoring to see if the deal fits the DSCR lender box before you submit. No email. No sales pitch.

If you want the “lender brain” in one place

Download the DSCR Playbook (PDF) and use the DSCR Loan Pre-Submission Checklist before you send a file to any lender.

Want a second set of eyes on your deal?

If you’re unsure why a deal feels “close” but not clean, request a review. We’ll tell you what will likely get conditioned, repriced, or declined.

Already working a deal?

No Hype. Just Real Numbers.

BKDSCR is an independent DSCR education and advisory platform. We do not originate loans or act as a mortgage broker. BKDSCR may receive compensation from partner lenders when a client introduction results in a closed loan. This does not affect the independence of our analysis or deal review process.