Most investors analyze deals from their own perspective: What’s the rent? What’s the payment? Does it cash flow? That’s a reasonable starting point. It’s not how underwriters think.

Lenders evaluate DSCR deals in a specific sequence — a triage framework designed to eliminate risk at each stage before committing resources to the next. Understanding that sequence doesn’t just help you anticipate objections. It changes how you structure, present, and defend your deals.

This page walks through the lender’s order of operations: the four stages every DSCR deal moves through from submission to approval, what gets evaluated at each stage, and where the process most commonly breaks down. This isn’t a spreadsheet. It’s the decision logic underneath the spreadsheet — the framework that determines whether your numbers even get looked at.

Step 1: Does the Deal Cash-Flow on Paper?

STAGE 1 — INCOME VS. DEBT SERVICE

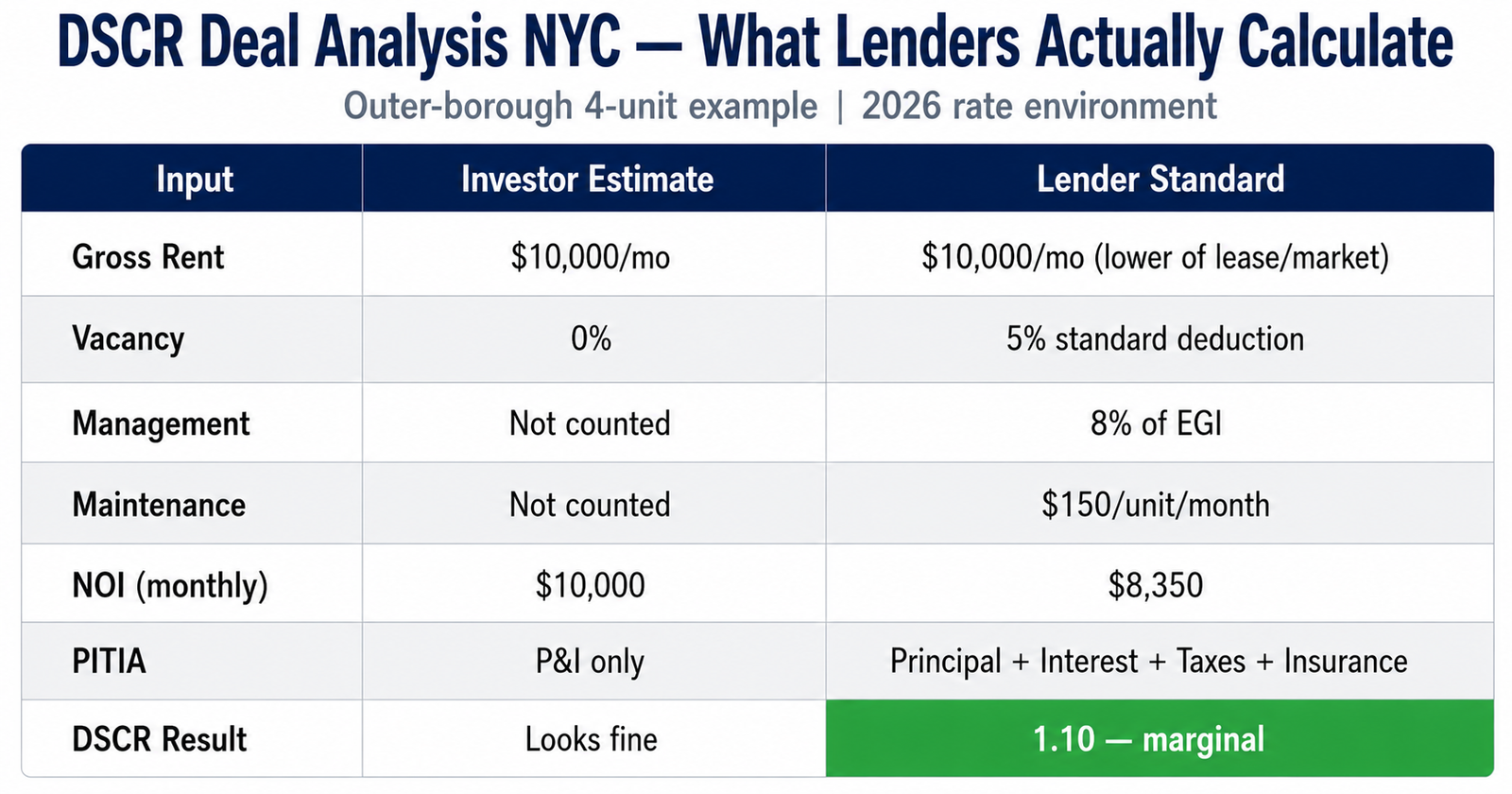

The first thing an underwriter does is check whether the property’s income covers its obligations. This is the DSCR calculation — but from the lender’s side, not yours.

How underwriters build the number

The underwriter isn’t looking at your pro forma. They’re looking at documented income — the existing lease amount or the appraiser’s fair market rent opinion, whichever is lower — against the fully loaded debt service: principal, interest, taxes, insurance, HOA, and any other recurring property-level obligations.

They’re applying a vacancy factor. They may be including property management fees regardless of whether you use a manager. The number they calculate is almost always lower than the number you calculated.

The Investopedia definition of net operating income covers the general formula — but for DSCR analysis, lenders apply a specific version that includes vacancy, management, and maintenance deductions that most investors omit from their initial underwrite.

This stage is binary. If the deal doesn’t clear the lender’s minimum DSCR threshold, nothing else about the deal matters — the file stops here.

What kills deals at this stage

Rent assumptions that don’t survive the appraisal. You modeled $2,200/month. The appraiser’s rent schedule supports $1,900. The DSCR compresses and the deal needs restructuring — or it’s dead.

Debt service calculated without the full PITIA load. You quoted P&I only. Taxes, insurance, and HOA add $600/month to the denominator. The ratio drops below threshold.

IO vs. amortized mismatch. You calculated at the IO payment. The lender qualifies on fully amortized debt service. Two different ratios, one deal.

Bottom line: The underwriter’s first question is simple: does this property pay for itself under their assumptions — not yours?

Step 2: Does the Market Support the Rent?

STAGE 2 — RENT DURABILITY AND MARKET RISK

Once the DSCR clears on paper, the underwriter asks a harder question: is the income figure reliable? A ratio based on rent that’s inflated, unsustainable, or vulnerable to market shifts isn’t a real ratio. It’s a snapshot that can’t be trusted to hold.

What lenders examine in the market check

Rent comparables. The appraiser provides rent comps as part of the 1007 rent schedule, and the underwriter evaluates whether those comps support the income figure being used. If your in-place rent is significantly above comps, expect pushback.

Rent volatility. Markets with sharp recent rent increases draw scrutiny. Underwriters know rapid rent growth often corrects. They ask: if rents flatten or pull back 5–10%, does this deal still work?

Short-term rental risk. Even lenders who accept STR income typically apply conservative assumptions: lower occupancy, discounted nightly rates, and sometimes blanket reductions to modeled income.

Declining or transitional markets. Population loss, employer departures, rising vacancy, and falling values shift underwriting posture. Some lenders apply explicit market overlays; others use discretion to condition or decline.

DSCR measures the deal at a point in time. Underwriters evaluate whether that point in time is representative — or an aberration.

Step 3: Does the Structure Survive Stress?

STAGE 3 — STRUCTURAL RESILIENCE

A deal that cash-flows today with income the market supports still has to survive the scenarios the lender models. This stage is about structural durability: what happens to the deal when conditions change?

What gets stress-tested

Rate sensitivity. If the loan is adjustable-rate, the underwriter models what happens at the first adjustment and potentially at the cap. Some lenders qualify at start rate; others qualify at a fully indexed or stress rate.

Exit risk. Even fixed-rate deals can fail at the exit: if you plan to refi in five years and rates are 100 bps higher, the refi DSCR may not support the same leverage.

Interest-only roll-off. IO improves near-term cash flow, but creates a payment cliff when amortization begins. Underwriters want to see you understand that cliff and have a plan.

Expense creep. Taxes, insurance, and HOA don’t stay static. Underwriters anticipate reassessments and premium increases — especially in storm, wildfire, or coastal exposure markets.

A deal that works under current conditions and fails under reasonable stress scenarios is fragile. Structure your deal to survive the stress test — not just pass the base case.

Step 4: Are There Hidden Disqualifiers?

STAGE 4 — CRITERIA AND OVERLAY SCREENING

A deal can pass every analytical test — strong DSCR, defensible rent, resilient structure — and still fail on criteria that have nothing to do with the economics. This is where lender-specific policies, overlays, and guideline technicalities either confirm the deal or stop it.

Disqualifiers that don’t show up in spreadsheets

Property-level disqualifiers. Property type restrictions, condition requirements, geographic exclusions, loan size limits, and seasoning rules are binary gates.

Borrower-level disqualifiers. Credit floors, reserve shortfalls, concurrent loan limits, and experience requirements can stop an otherwise sound deal — and these criteria compound.

Structural disqualifiers. LTV caps, IO eligibility limits, and prepay structures incompatible with your timeline can kill the deal-to-lender pairing.

Final Step: Match the Exit Strategy to the Loan Structure

A deal can pass cash flow, market validation, stress testing, and criteria screening — then still cost you money later if the loan structure does not match the exit. This is where many investors focus too much on rate and not enough on prepayment penalty exposure.

Prepayment Penalty Selector

Choose the most likely exit timeline. The recommendation updates automatically.

Pre-Screen Before Submitting

The lender’s order of operations isn’t a secret. The four stages on this page are the same four stages every DSCR deal moves through. The difference between investors who close efficiently and investors who burn cycles is whether they run their deal through this framework before the lender does.

Every variable is checkable in advance: the DSCR under lender assumptions, the durability of the rent, the structural resilience under stress, and the criteria fit for the specific lender.

If you want to run your deal through this framework before submitting it — checking the DSCR, the market support, the structural resilience, and the criteria fit in one pass — the 60-Second DSCR Deal Filter does exactly that.

Or get the complete analysis framework in one document

The evaluation sequence, the lender criteria, the deal killers, and the math behind every stage — all in one place.

Already working a deal?

No Hype. Just Real Numbers.